by Julian Lee* OPEC's strategy to lock down its share of the oil market comes with a worrying by-product: rising production means the world is less able to cope with a big supply disruption than at any time since the financial crisis. That may not seem a cause for fear when the world's awash with oil. But it could become much more of a problem once the market re-balances and demand outstrips supply again

OPEC's strategy to lock down its share of the oil market comes with a worrying by-product: rising production means the world is less able to cope with a big supply disruption than at any time since the financial crisis.

That may not seem a cause for fear when the world's awash with oil. But it could become much more of a problem once the market re-balances and demand outstrips supply again.

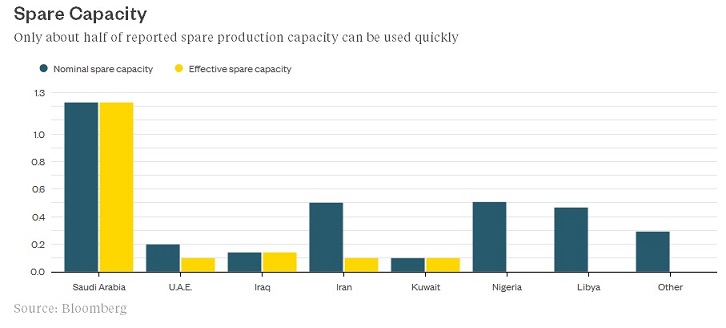

Global spare capacity -- defined by the IEA as the volume of oil that can be brought into production within 90 days and sustained for an extended period -- stands at 3.44 million barrels per day, according to data compiled by Bloomberg. But much of that may not be available as quickly as you'd hope. Libya's 500,000 barrels of spare daily capacity, for example, can be used only if the political situation improves enough to allow unrestricted exports and secure access to fields and pipelines.

Almost all usable spare capacity is held by Saudi Arabia. Deputy Crown Prince Mohammed bin Salman told Bloomberg in April that his country could raise output to 11.5 million barrels a day immediately; lifting it to 12.5 million barrels would take six to nine months.

To this, we can probably add 100,000 barrels each from Abu Dhabi, Kuwait, Iran and Iraq. But that's about it: 1.7 million barrels per day of immediately available capacity.

This is dwarfed by some of the losses we've experienced. The biggest was the loss of 5.6 million barrels per day for six months during the Iranian revolution. Even more disruptive was Iraq's 1990 invasion of Kuwait, depriving the world of more than 4 million barrels of daily supply overnight. It took more than three years to restore Kuwait's pre-invasion output. Iraq's didn't recover fully for almost 20 years.

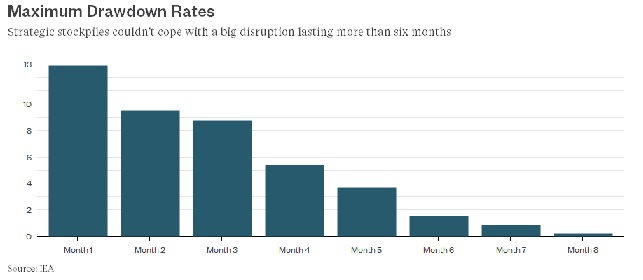

Strategic and commercial stockpiles provide some security, but they're a one-off. Once drawn down, they're gone. The OECD countries have about 1.6 billion barrels of crude and refined products in government-controlled storage and almost twice that in industry stockpiles. More more than enough, in theory, to offset a three-year loss of Kuwait's production.

But it's not that simple. Much of the commercial inventory is needed to keep pipelines and refineries running, so can't be used. As well as issues of quality and location, there's the problem of how quickly oil can be drawn from storage. In 2005, the IEA reported that government-controlled inventories could be drawn down at an initial rate of nearly 13 million barrels per day, but only for a month. By month six that falls to about 1 million barrels and by the eighth it's a trickle (nowhere near enough to cope with a major, prolonged loss of supply.)

So where is production most at risk? In several places. Venezuela's economy is reeling and oil output is falling. Social unrest could lead to another strike like the one that crippled production in 2002-2003. Islamic State militants have attacked fields in northern Iraq, though they'd need a successful strike against export facilities in the south to really impact supplies.

However, it's Nigeria that's emerging as the prime candidate for disruption. Output has suffered because of unrest in the Niger Delta region, with a new group, the Niger Delta Avengers, claiming credit for a string of raids. Chevron's 50,000-barrel-per-day Okan offshore facility was attacked on Thursday night, while the 300,000-barrel-per-day Forcados export terminal was closed in February and may not reopen until next month.

There's no shortage of production at risk and a dwindling amount of spare capacity to compensate. This is far from an academic concern.

*Julian Lee is an oil strategist for Bloomberg First Word. Previously he worked as a senior analyst at the Centre for Global Energy Studies.