HELLENIC PETROLEUM Group reported its strongest 4Q performance, leading to a FY adjusted EBITDA of €417m (2013: €178m) and recording a positive Net Income. Performance was improved in all business units, some of which reported record high contribution. In refining, results were driven by the favorable international refining environment during the second half of the year, as well as improved refining operations, following the de-bottlenecking works at Elefsina earlier in the year. Further support came from continuous cost control efforts and growth in exports, accounting for c. 50% of total sales.

Contribution of marketing activities was also higher: EKO and HF profitability came in at 4-year high, as a result of the transformation initiatives implemented over the last two years. The Group’s international subsidiaries reported their highest contribution ever, despite challenging local market conditions. Finally, Petrochemicals also improved performance, with record high profitability.

Reported results were severely affected by the sharp decline of crude oil prices, impacting year-end valuation of inventory. As Hellenic Petroleum maintains a high inventory level as part of its Compulsory Stock Obligations, the total loss from the price drop in 2014 was €484m, turning positive operating results for the year to a Net loss of -€365m.

Group cashflow was also positive, as, during the last quarters, increased profitability, combined with normalised capex levels, led to reduced leverage. In terms of funding, despite the continued challenges, the Group’s position improved following the Eurobond issues and the renegotiation of existing credit facilities. Strategic targets on both tenure (maturity profile) and diversification (DCM vs Banks) have been achieved and interest costs are gradually being reduced. Given continuing market volatility, the management of liquidity risk and security of supply for our core markets remain key priorities and these are being addressed by holding a relatively high average cash balance, with a commensurate negative impact on interest costs.

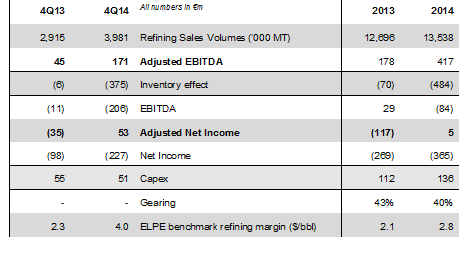

Capital expenditure, at €136m, mainly relates to stay-in-business projects, the turn-around of Elefsina and smaller growth projects.

Key figures for 4Q and FY 2014 are summarised below:

Significant drop in crude oil prices and further improvement of European benchmark refining margins; stronger dollar vs euro in 4Q14

Global oil supply surplus continued in 4Q14 mainly due to increased production in US and Iraq and OPEC’s decision to maintain its output unchanged. As a result, crude prices dropped to their lowest since May 2009, with January 2015 Brent crude oil price falling below $50/bbl; a decline of $45/bbl in 4Q14 and more than $65/bbl in 2H14.

US dollar strengthened further vs euro q-o-q, with a positive effect on $ driven benchmark margins. Euro averaged $1.25 in 4Q14, the lowest since 2006.

Reducedenergy costs, due to weak crude prices and lower diesel imports from North America were among key factors that supported benchmark margins improvement during 2H14, reversing the challenging environment of the first half. Benchmark Med FCC margins averaged $3.4/bbl, (2013: $2.4/bbl), while Hydrocracking came at $4.5/bbl (2013: $3.7/bbl).

Demand growth in domestic fuels market

Domestic fuels demand in 2014 amounted to 6.7 million tones, according to preliminary official market data, recording a 1.5% growth, for first time since 2009. Diesel consumption increased, outweighing gasoline demand reduction, with diesel cars accounting for 60% of new car registrations. Furthermore, low prices coupled with the reduction of excise duty led to a 5% increase in the demand for heating gasoil.

Strong operating results in 4Q14

Group Adjusted EBITDA came in at €171m (4Q13: €45m), reflecting mainly the enhanced contribution from refining operations. Elefsina refinery rebased its contribution, with high utilisation rates and consistent over-performance throughout the quarter. Furthermore, both Marketing and Petrochemicals increased contribution.

The large drop in crude oil and product prices resulted in inventory losses of €375m, leading 4Q14 Reported EBITDA to -€206 (4Q13: -€11m), while Net Results amounted to -€227 (4Q13: -€98m).

Operating cashflow was positive for the second consecutive quarter, reflecting both improved performance and normalized capex. Net debt at €1.1bn, lower vs last year, with gearing at 40% (4Q13: 43%). In 4Q14, the Group renewed c.€1.5bn credit facilities with Greek banks, further improving commercial terms, maturity and cost. Moreover, in the first weeks of 2015, the Group signed a 3-year, €200m revolving credit facility, which further added to the cash balance.

Regarding the sale of 66% of DESFA share capital to SOCAR, the regulatory approval is in progress, with the approval of the European Competition Authorities being the final step for the completion of the regulatory clearance.

Exploration and Production in Greece

On 6 February 2015, HELLENIC PETROLEUM submitted offers for the lease of Arta-Preveza and NW Peloponnese areas in West Greece, following a relevant tender by the Ministry of Production Restructuring, Environment & Energy. In the West Patraikos Gulf area, where HELLENIC PETROLEUM acts as operator in a JV with Edison International SpA and Petroceltic Resources Plc, exploration activities have started.

John Costopoulos, Group CEO, commented on 4Q14 performance:

"In the fourth quarter, the Group reported strong operating profitability, on better global refining environment and the improved performance of all business units.

During 2014, Hellenic Petroleum realized the benefits of the strategic transformation projects implemented over the last few years such as (a) the upgrade of the refineries, (b) competitiveness improvement and (c) retail business model transformation. Indications of this performance are the achievement of the highest ever production volume and exports sales, as well as the over-performance of our refineries vs benchmark margins. Furthermore, in 2014 we successfully completed the refinancing strategy and managed liquidity and credit risks, despite the continuous challenges and volatility for Greek corporates.

In line with all refiners who hold significant inventories, the negative impact of crude oil price affected our otherwise strong results.

For 2015, we

plan for an equally challenging environment, as commodity markets volatility,

the start-up of new competitive refineries in the Middle East and uncertainties

in the economy are expected to continue. HELLENIC PETROLEUM will continue to focus

on competitiveness, operational excellence and prudent management of business

and financial risk, to deliver sustainable benefits for our shareholders,

personnel and all stakeholders.”