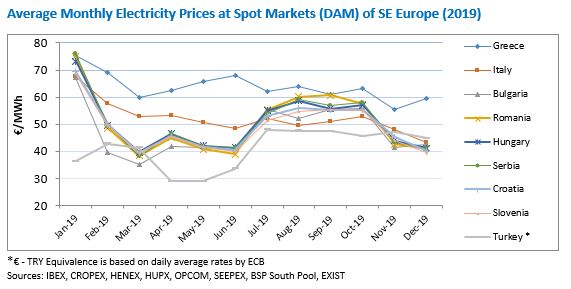

According to a recent report by the European commission wholesale electricity prices in the Greek market were the highest in Europe in the first quarter of 2020. Even though this is a problem that has recently caught the attention of Greek authorities and press, it is an ongoing issue, that was intensified in 2019.

The main reason for the upward trend of wholesale electricity prices in Greece in recent years is the gradual loss of competitiveness of domestic lignite-fired power generation, as a result of the high operational costs and the gradual increase of carbon emission allowances in the Emission Trading System (ETS). At the same time, lignite plants have to face the increasing competitiveness from imports and domestic gas plants, as a result of lower gas prices in recent years and especially in the second half of 2019, as a result of high competition due to the differentiation of the origin of imports. In addition, the flexible production of gas units has become increasingly necessary for balancing variable renewables. The significant drop of gas prices over the past decade (2010-2019), has also driven their higher penetration in Greece’s electricity mix, with the most significant increase recorded in 2016, when power generation from gas units marked the largest annual increase of the decade, at 67% compared to 2015.

Also, the gradual penetration of RES in the electricity mix from 6.5% in 2012 to 20.6% in 2019 significantly reduced the available space for baseload electricity generation, making it increasingly difficult to integrate lignite units in the daily planning of electricity generation, given their relatively high generation cost. Moreover, the cost of emissions allowances (ETS) has risen significantly since 2012, with its price rising sharply from 2018 onwards. The price of emission allowances more than tripled, coming close at € 25 / ton (ton CO2 eq.) at the end of 2019, from € 7.5 in March 2012 and as a result has sent the operating costs of lignite plants soaring. This makes gas units extremely competitive, achieving increasingly low variable operating costs due to major producers securing LNG supply at low cost.

In addition to natural gas units, extremely competitive imports assisted in balancing wholesale electricity prices throughout 2019. More specifically, net electricity imports in Greece increased due to the significant reduction of electricity demand in neighboring markets, such as Italy and Bulgaria, which fell by 3.1 TWh (-1% y-y) and 0.7 TWh (-1.8% y-y) respectively. At the same time, baseload power generation in the region became highly competitive due to the significant increase in ETS prices in 2019, as Romania, Bulgaria and the countries of the Western Balkans (see Serbia, Bosnia and Herzegovina, etc.) did not participate in the European emission trading mechanism (ETS) and therefore did not incorporated costs for their emissions to the variable costs of their domestic thermal power plants. This situation facilitated the increase of the net imports in the Greek system by 62.4% in 2019, marking a decade high at 9.74 TWh or 19.28% of the total demand of the system. Consequently, electricity imports in Greece now account for an average of 21% (June 2020) of the electricity mix.

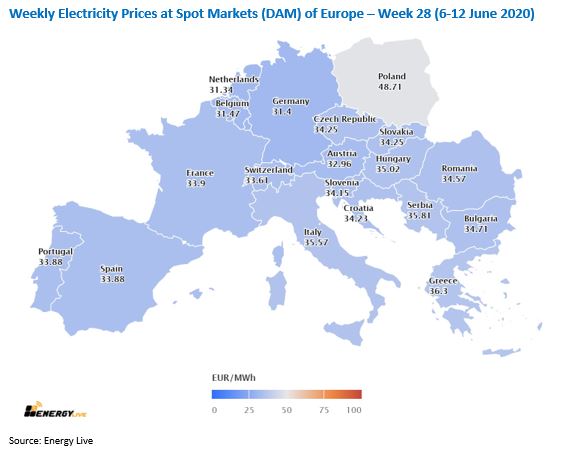

Although import prices were competitive, they were not that low, as they represented generation in neighboring markets, in which wholesale market prices are defined by lignite-based and gas-fired units, such as Bulgaria and Italy respectively. In comparison, we can observe a market that is more dependent on imported electricity than Greece like Hungary, which imported 27.8% of its needs, in order to cover the domestic electricity demand in 2019. Wholesale electricity prices in the Hungarian wholesale market (HUPX) were lower by 26.9% ( - €13.53 / MWh) than in Greece and this is because its imports came from markets whose wholesale prices are largely determined by RES and nuclear power, such as Austria-Germany and Slovakia, Ukraine respectively, i.e. from generating units with extremely low to zero variable costs.

One should further note that, most of the volumes of electricity traded in regional wholesale markets, except Greece, do not exceed 40-60% of the total volume of domestic electricity demand, meaning that the actual cost of electricity in each country is not fully presented at wholesale level, as currently applies in Greece. In addition, regional markets like Italy and Romania, participating in Multiregional Coupling (MRC) and 4MMC market schemes respectively see the results of their markets being formulated by the generation mix with the lowest cost at regional level via implicit cross border trading, which is not the current practice in Greece today. With market coupling with Italy and MRC expected as soon as 2021, after the application of the target model market initiative in the Greek electricity market, which starts next September, there are hopes for a modest decrease of wholesale electricity prices in the Greek electricity market.

Finally, we should mention that wholesale electricity prices in Greece have already seen a decline in the second quarter of 2020, affected by a significant decline in demand due to the imposed measures to mitigate the spread of Covid-19. As a result, Greece lost its first place for the highest wholesale electricity price in Europe to Poland. IENE is closely monitoring the performance of regional and European wholesale electricity markets through its weekly publication SEE Electricity Market Analysis, which is only sent to its members. In this newsletter, the Institute is presenting the electricity price trends in Bulgaria, Croatia, Greece, Hungary, Italy, Romania, Serbia and Turkey, on a weekly basis, analyzing the performance of the electricity sector with regard to generation and cross-border electricity trade.