by Costis Stambolis* As the "Energy Union”, EC‘s latest ploy in its bid to force member states to adopt a common energy policy is fast gaining ground, having already celebrated its first anniversary, so is mounting opposition to this pharaonic plan from several governments which have well developed energy strategies of their own

As the "Energy Union”, EC‘s

latest ploy in its bid to force member states to adopt a common energy policy

is fast gaining ground, having already celebrated its first anniversary, so is

mounting opposition to this pharaonic plan from several governments which have

well developed energy strategies of their own. Enthusiastically backed by Maros

Sefcovic, EU’s ambitious vice president, and considered by many to be the main

architect of the Energy Union concept, one of its prime goals, along with

maximizing the use of RES and Energy Efficiency, is the strengthening of

European security of energy supply by means of diversification of supply

sources and ultimately the lessening of EU’s dependence on Russian oil and gas

imports.

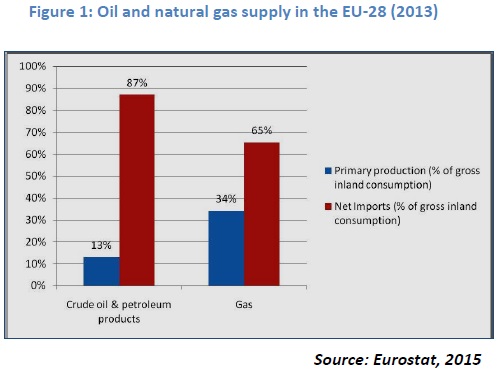

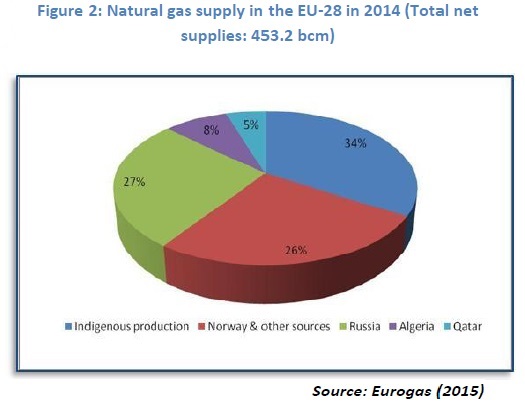

Although it is true that EU28 depend on Russia for about 40% of their crude oil and 33% of natural gas imports, the rest of the hydrocarbon imports pie is well spread between a multitude of countries ranging from Algeria, Norway, Nigeria and Qatar for gas to Saudi Arabia, UAE, Iraq and Iran and many others for oil (see Fig. 1 and Fig. 2). However, the greatest problem which EU faces with regard to its oil and gas supply is its huge hydrocarbon import dependency per se as indigenous production represents a paulty 13% for oil and a little more than 30% for gas. So EU’s energy supply problem has more to do with its failure to produce enough oil and gas from indigenous resources rather than its forced dependence on oil and gas imports . Admittedly, gas is the fastest growing fossil fuel supported by strong supply growth, particularly of US shale gas and liquefied natural gas (LNG), and by environmental policies and hence EU’s interest in promoting further the case of LNG appears justified. Given that this forced EU dependence on gas imports appears to be the main concern in the minds behind the Energy Union, it is strange, if not incoherent, that they seek to broaden this dependence by encouraging the escalated use of LNG which is of course totally imported. In doing so European Union advocates a rapid expansion of LNG terminal construction across Europe, in order to increase import capability. This is already happening if we look at latest additions in Lithuania, Italy and plans for new LNG terminals, especially floating ones in Greece, Croatia and Turkey.

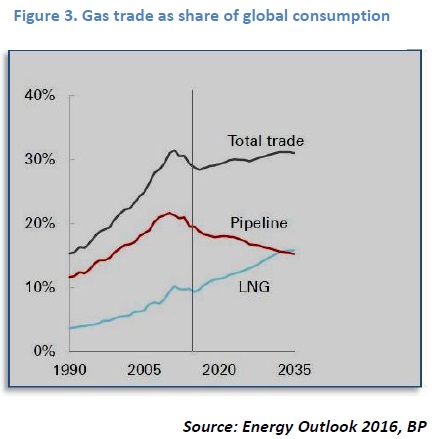

As BP points out in its latest 2016 Energy Outlook Report, international trade in gas grows over the next 20 years broadly in line with global consumption, such that the global trade share of gas remains around 30%. But within that, LNG trade grows twice as fast as consumption, with LNG’s share of world demand rising from 10% in 2014 to 15% in 2035. Over 40% of the increase in global LNG supplies is expected to occur over the next five years as a series of in-flight projects are completed. This equates to a new LNG train coming on stream every eight weeks for the next five years! By 2035, as BP’s scenario indicates, LNG surpasses pipeline imports as the dominant form of traded gas (see Fig. 3). The growing importance of LNG trade is likely to cause regional gas prices to become increasingly integrated. Furthermore, the growth in LNG coincides with a significant shift in the regional pattern of trade. The US is likely to become a net exporter of gas later this decade, while the dependence of Europe and China on imported gas is projected to increase further.

Today EU28 imports some 50bcm of LNG which

corresponds roughly to 12.5% of its total gas consumption. Even if this number

was to double by say 2025 or sooner, EU would still cover only 20% of its total

gas needs from LNG, assuming that gas consumption rises at least by 5%-6% by

that time. Although by increasing LNG supply EU will inevitably increase

further its energy import dependence. But according to the mindset of Energy

Union bosses this is not necessarily a negative prospect since some of the LNG

will eventually start coming from USA and Canada, which will soon become major

LNG exporters, and which apparently are more friendly and supportive to EU’s ideas and policies

than the "bad”, or even threatening, Russians are.

So the game boils down to sheer politics, although EU bureaucrats will never openly admit it, and is based on deep rooted misconceptions going back to the cold war and the Iron Curtain. But as energy in almost all its forms is now a global commodity and hence its trading follows market trends, the problem with EU’s aggressive pro LNG policies is that they may soon backfire since EU28 will find itself in the uncomfortable position of having to increase, rather than decrease, its dependence on Russian gas. Since Gazprom and other Russian companies, such as Novatek, shall over the next 3-4 years start exporting a lot more LNG volumes than they currently do. And as LNG production is bound to increase in the coming decade, as a whole string of new liquefaction plants comes on stream, so will prices converge with those of piped gas. And as to where from EU countries will import their LNG, this is a decision governed entirely by market fundamentals and company profitability priorities- as LNG is a freely traded commodity- rather than dictat from Brussels; whose functionaries are obsessed with central planning and grandiose strategies, a relic of the now bygone Soviet Union era. And in that respect there appears to be a striking similarity between old Soviet economic methods with present day Energy Union masterplans.

In conclusion, one is very much tempted to observe that increased LNG imports to EU is not necessarily a bad prospect but it will by no means solve the continent’s gas import dependency nor contribute greatly to diversification of gas supply origin. However, where increased LNG use in the EU will help is towards gas market versatility, gas price convergence and greater competition which should theoretically lead to lower prices and will also benefit the consumer.

*Costis Stambolis is the Executive Director of the Institute of Energy for SE Europe

Source: "IENE Comment", April 9, 2016