One of the EU’s most ambitious infrastructure projects is getting closer to realisation, as a crucial decision looms on the route to be selected of a new major gas pipeline which will bring gas from the Caspian to the heart of Europe.

One of the EU’s most ambitious infrastructure projects is getting closer to realisation, as a crucial decision looms on the route to be selected of a new major gas pipeline which will bring gas from the Caspian to the heart of Europe. By the end of the month, a BP-led consortium developing a massive gasfield off the coast of Azerbaijan called Shah Deniz II must decide on the optimum gas route for gas to be delivered to Europe.

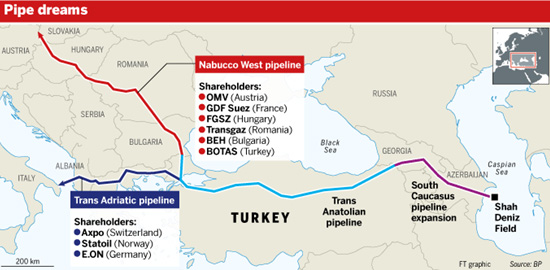

The Shah Deniz partners must decide between two rival projects: one going to Austria, called Nabucco West, and the other ending in Italy, called the Trans-Adriatic Pipeline, or TAP. As the FT observed in a recent article "behind those dry facts lies a long, combustible saga of geopolitical intrigue, bitter corporate rivalry and intense debate about the future of Europe’s energy need. It has been a hard-fought battle in which some of the continent’s largest energy companies have devoted vast resources to complex commercial negotiations, delicate great-power diplomacy and intense lobbying from Brussels to Baku. And the outcome is too close to call”.

Competition is running high since both pipeline projects are well developed from an engineering point of view while both present significant market opportunities for the gas quantities which they will be transporting.

The decision will mark a crucial milestone for the EU as it struggles to improve its security of supply. It will bring it a step closer to tapping a brand new source of natural gas, at a time of declining indigenous production and forecasts of rising demand as the continent turns its back on polluting coal. However, gas is not expected to begin flowing before 2019.

The Shah Deniz II field and the associated pipelines have been developing as viable projects over a decade. Both the Caspian gas field and the pipelines are considered as bold and expensive endeavours. It is estimated that the whole venture will cost upwards of $40bn – $25bn for the development of the Shah Deniz II field itself and at least $15bn for the delivery system, including a huge new pipeline called Tanap that will pass through Turkey. Though neither TAP nor Nabucco West has disclosed a price tag, analysts estimate that each could cost as much as $5bn.

And yet there are big doubts as to how much difference the new pipeline will make. Shah Deniz II will provide Europe with 10bn cubic metres a year of gas – equating to just 2 per cent of total European demand. Gazprom, the Russian gas giant, will supply Europe with more than 15 times that amount this year. Privately, Gazprom managers dismiss the Azeri gas as "just about enough for a barbecue”.

But others say that misses the point: that once the pipeline is built, more supplies will become available. Azerbaijan itself has made some big gas discoveries in the Caspian Sea in recent years that could feed into it. A number of significant new gas deposits have been identified on the Azeri Caspian Sector including the Umid, Shafag - Asiman and Nakhichevan fields.

Today, the duel between the two rival projects is one between a long-established heavyweight and an upstart. Named after a Verdi opera, Nabucco was first conceived back in 2002. At the time, the EU was actively exploring options for a "southern corridor” that would bring gas from Central Asia and the Middle East and reduce the continent’s dependence on Russia: so Nabucco quickly won strong backing from Brussels. TAP, a much slimmer and more savvy project, came later.

Nabucco’s managing director Reinhard Mitschek says the issue of diversification is crucial. "If you look at south-eastern Europe and the western Balkans, the countries in this region are at least 50 per cent dependent on Russian gas,” he says. That is not the case with TAP’s target destination, he says. "Italy is quite a diversified market.” But some analysts say that argument is no longer relevant. In the past few years, Europe has invested heavily in interconnectors that link up the gas grids of EU member states, in part to prevent future supply disruptions. There is a whole group of such gas interconnectors to be soon constructed in SE Europe including the Greek – Bulgarian interconnector and the Turkish – Bulgarian one.

However, "The strategic importance of Nabucco has been reduced because of the flexibility of the European gas market,” says John Roberts of Platts, author of "Pipeline Politics: The Caspian and Global Energy Security”. Most analysts agree that lately the European Commission has been siding in favour of TAP. Many in Brussels support it because by passing through Greece it could give a big boost to the country’s crisis-hit economy, providing jobs, transit fees and cheap gas.

TAP has other advantages, too: "It allows you to access virgin markets such as Albania, Montenegro, and possibly Kosovo,” says Michael Hoffmann, TAP’s head of external affairs. In this context the TAP construction has well developed plans for the construction of IAP, in the Ionian Adriatic Pipeline, which will bring gas to the West Balkans which until now have no access whatsoever to gas supplies. He also says TAP can hook up with other pipelines that would potentially extend its reach into Austria and even the UK.

Ultimately, the decision will be based on commercial considerations alone note industry sources familiar with both projects. The Shah Deniz partners are talking to buyers along the routes of both pipelines to see what they are prepared to offer for Azerbaijan’s gas. Analysts say there are indications of greater appetite along the TAP route than along Nabucco West’s.

At the same time sources close to Socar’s management in Baku observe that the Azeri national oil and gas company which has a significant stake in the whole project is rather sensitive of the political and diplomatic implications involved in the gas pipeline selection process. In this sense they (i.e. Socar) is pushing for a two phased solution whereby it will prioritise TAP in terms of construction timetable while it will retain Nabucco for a second phase, pending the development of the new Azeri gas fields in the Caspian from where fresh gas supplies are expected to start flowing after 2023.

The question remains if such an outcome will be acceptable to the Nabucco partners who have been patiently developing the project over the years by pumping not insignificant amounts of money.

(source: IENE’s SOUTH-EAST EUROPE ENERGY BRIEF- Monthly Analysis, Issue No 98 • June 2013)