Mr. Simon Bennett, Energy Technology Analyst of the Paris-based International Energy Agency (IEA), was a keynote speaker at the “Innovation in Energy” Conference, held by the Institute of Energy for SE Europe (IENE) on May 8, 2025, at the prestigious Cotsen Hall in Athens.

This latest IENE conference examined the critical role of innovation in energy transition and also helped launch the Institute’s “Innovation in Energy” programme, which was presented during the event. As Mr. Bennett stressed at his video message, through which he addressed the conference, the objectives of both this new programme and conference by IENE are closely aligned with those of his team at the International Energy Agency in Paris and also with his own personal enthusiasms.

He also presented some messages from the State of Energy Innovation Report that IEA published just one month ago, with input from experts all around the world, which included a range of data sources and metrics aiming to illustrate the importance of innovation.

The video of the presentation by Mr. Simon Bennett (IEA) at IENE's "Innovation in Energy" Conference, on May 8, 2025:

Here follows the full transcript of Mr. Bennett’s address to IENE’s “Innovation in Energy” Conference:

“Good morning, Mr. Secretary General, Mr. Chairman, and all participants at today's conference. It's a great pleasure to be invited to provide a short address to this event. But of course, I do so with some regret that I cannot join you in person to congratulate IENE on the launch of the “Innovation in Energy” programme. The objectives of this new programme and today's conference are closely aligned with those of our team at the International Energy Agency in Paris and also with my own personal enthusiasms.

We look forward to being able to learn from you as a partner in Southeast Europe about exciting new energy technology developments in the region and about opportunities for international cooperation. The IEA itself, an intergovernmental agency that counts Greece among our members, has a mandate to help governments understand the latest technology trends and help them to work together to implement policies and programmes that support innovators in a range of ways to contribute to strategic policy objectives.

These include energy security, competitiveness, environmental protection, climate change, and energy access around the world. We cover all energy technologies including power grids, hydrogen, artificial intelligence, energy efficiency, and nuclear. All the topics that you will be delving into today.

However, we often find that decision makers do not have awareness of the importance of supporting technology innovation as part of an overall energy strategy. They don't always know about the latest policy approaches being implemented in different countries. They often don't have a robust overview of all the impressive areas of technological progress that we track here at the IEA. Not only the radical but also the incremental elements of progress. And that's a problem because intangible outputs do not easily get the attention of decision makers and there is always a risk that they are cut back at times of competing priorities such as today.

Against this backdrop, in our new “State of Energy Innovation” report that we published just one month ago, we assembled a range of data sources and metrics to illustrate the importance of innovation, to highlight progress, and to identify potential action areas. All to assist decision makers in making the right choices that can help deliver on the key policy goals of tomorrow.

And I'd like to present a few messages from that report which we put together with input from experts all around the world. including from our technology collaboration programmes at the IEA and via a survey of 300 practitioners that we conducted at the end of 2024. In fact, we'd be delighted to be able to include some of you in future editions of such an exercise. Let me begin my presentation of some of the findings from the report with a reminder that the benefits of technology innovation for the energy sector often reveal themselves only in hindsight after successful commercialization. But the seeds are always sown earlier.

Let me give you three examples.

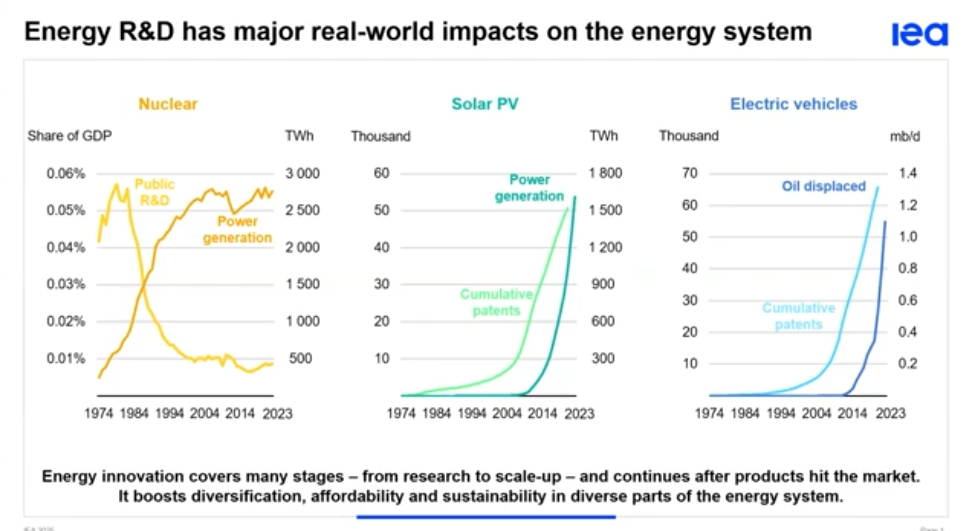

Nuclear energy is today a mainstay of global electricity generation and much of it was deployed in the years following the 1970s oil crisis. It is perhaps less well known that the growth was fueled by research. In response to the energy crisis, by 1980, IEA governments were spending nearly 0.06% of their GDP on public nuclear energy R&D, a higher share than they spend today on all energy R&D combined. The benefit for the energy sector has been tangible. Nuclear helped moderate oil and gas demand for power plants and diversified energy use.

At the other end of the spectrum of power generation in terms of scale and accessibility, solar PV has become the cheapest new source of electricity in most countries of the world in recent years, driving its exponential adoption. In 2024, generation from solar PV rose by 480 terawatt hours, more than the total annual electricity demand of Indonesia.

This outcome did not fall from the sky. Of course, the journey of modern solar PV from a first prototype in the 1950s, the largest source of global capacity additions, was accompanied by continual innovation. And that's indicated here on the slide by the patenting that preceded deployment.

So yes, policies to support PV deployment and the massive scale-up in manufacturing facilities especially in China have been critical success factors but its roots are very much in innovation.

And a similar pattern can be seen for electric vehicles and the oil demand that has been saved after the inflection point for cumulative invention. Solar PV and electric vehicles have built on widespread private sector innovation efforts to capture market share, including in countries that were not previously major energy R&D hotspots.

While the main sources of new energy technologies historically were large western economies, including more recently Korea, the patenting of those regions, despite being relatively high and relatively constant, has been shocked by recent patent data that we've been looking at that shows how China has risen very, very rapidly to become the world's top country for annual energy patents. The overwhelming majority of China's patenting in the energy area is actually directed to areas that can be categorized as low emissions energy technologies. 95% of all its patents are now for low emission energy technologies. And we only have data that goes up to 2022 because there's a lag in patent data as many of you will know. And yes, we understand that patents are an imperfect measure of energy innovation for a number of reasons, but their trends are an important early indicator of priorities within countries and the direction of travel of innovation efforts.

Another interesting indicator that we've been looking at is global venture capital for energy. And it's worth commenting first on the just the remarkable level of growth that this chart shows up to 2022. And it feels like distant history now, but it should be recalled that in 2011 there was actually what was called a clean tech bust. and many investors lost money on startups that were not able to find markets for their products.

So, the main reasons why there was such a striking change in fortunes and a ramp-up from 2015 to 2022 relates to strong much stronger market expectations and we would pin much of this on policy announcements especially after the signing of the Paris agreement. But some of it also is related to continual cost declines for cornerstone technologies like solar PV and batteries which raised confidence in the ability of technology to de deliver results. And around from 2021-2022 we had a very low-interest rate environment that drew in more capital.

But that narrative now needs an update. Due to macroeconomic conditions, venture capital fundraising has fallen by about 20% for the last two years in a row. Now, there may be a good case for some consolidation in some areas, such as electric vehicle manufacturing, but overall, this decline is a risk for energy innovators. Over 1,800 startups raised equity in 2021 and 2022, and another 1,400 since then. If only a handful of these meet their scale up goals, it could have a significant impact on the energy system. But they will only scale up if they have access to operational capital.

Looking at the trend by technology area, we see that no area has been spared from the decline in the last two years. But there are bright spots. Nuclear, geothermal, and carbon capture utilization and storage are among the technology areas that raised more funds in 2024 than in 2023. And we can also use the data that we've gathered to make some comparisons. And while we know that different sources of funding play distinct roles in healthy energy innovation ecosystems, it helps to keep their relative sizes in perspective. Public research budgets which fund many of the innovations under development by startups continue to be larger than all global energy venture capital investing.

But so, we noticed something interesting about 2022. At the peak of energy venture capital, the difference narrowed almost to parity. But what's important here to notice is that the decline in venture capital since 2022 is perhaps a reminder that as a source of capital for innovators, it can be less reliable unless it is complemented by public R&D budgets that provide long-term continuity. And we are also well aware that there are other ways in which new technologies are invented, improved and nurtured towards real world impacts. Corporate research and development departments still actually spend more money on energy related R&D than public and venture capital combined. Now much corporate R&D is on vital incremental improvements and on product development, but that is no less important in a healthy energy innovation ecosystem.

So now I'm going to turn quickly to some uh other results that we've shown in the report that I think give a very positive message and that's about the innovation updates that we collected through expert solicitations and surveys and we're showcasing 156 different energy technology innovation highlights from the past year in the report and these manifest themselves in different forms. To illustrate this, perhaps the most obvious way to measure progress is to look at whether the innovation highlights have led to tangible improvements in technology. And we track this online in our energy technology guide. And in 2024, there were 65 different updates to that guide. And they include, for example, the first operating demonstration of an oxifuel kill to enable cement production with CCUS in China started operation in 2024. And it's expected by experts in the field that it could achieve commercial deployment by around 2030.

But there are also examples of innovation that represent other types of steps towards commercialization. In 2024, there was financial close for a major near zero emission steel making project in Sweden and that has hopefully brought its market uptake by the end of the decade within reach. Firm offtake agreements for small modular nuclear reactors in the United States may do the same in that technology area.

And some innovation highlights relate to the launching of new products that are already close to commercialization. In 2024, the world's first car powered by a sodium-ion battery hit the market, raising expectations for this innovative battery, which is made from commonly available materials and could be a possible complement to lithium-ion in some situations.

Overall, we hope that the report and any future additions will help to inform policymakers and innovators alike. There you'll find more information on policy updates, policy recommendations, some work on emerging economies and the needs in those regions, and three focus chapters. Those focus chapters are on innovation to diversify the sources of electric vehicle battery minerals, the use of artificial intelligence to accelerate energy technology innovation, and carbon dioxide removal.

I wish you every success with today's conference and with your new programmes. The IEA operates in between government, industry, investors, and academia, helping to build bridges among them. I look forward to following how your work contributes to these efforts and to perhaps meet some of you at future events. For example, at our IEA energy innovation forums that bring together a range of stakeholders to exchange views on the latest opportunities and on challenges.

Thank you very much”.