by Dr. Valery Nemov* The European gas market has gone through a substantial transformation. For several decades, this market was dominated by long-term contracts, derived from formula-based pricing. Market transformations resulted in the expansion of trading hubs and hub related pricing. The conventional wisdom is that gas hubs accurately reflect the balance of supply and demand in the whole European market, and the linkage between oil-indexed and hub prices has lost its rationale and does not reflect market fundamentals

The European gas market has gone through a substantial transformation. For several decades, this market was dominated by long-term contracts, derived from formula-based pricing. Market transformations resulted in the expansion of trading hubs and hub related pricing. The conventional wisdom is that gas hubs accurately reflect the balance of supply and demand in the whole European market, and the linkage between oil-indexed and hub prices has lost its rationale and does not reflect market fundamentals.

Gazprom Export research casts doubt upon this conventional wisdom. Our research has shown that although TTF (Netherlands) and NBP (UK) prices are reflective of supply and demand, they are, in essence, not independent and self-contained. They have a strong positive correlation with Gazprom’s oil-indexed prices, with coefficients of 0.75 and 0.79.

In that sense, hub prices are in fact derivatives of long-term contracts, which set the baseline trend for their development. Supply and demand only mutate their changes (see Blue Fuel, October Vol.6, p 11).

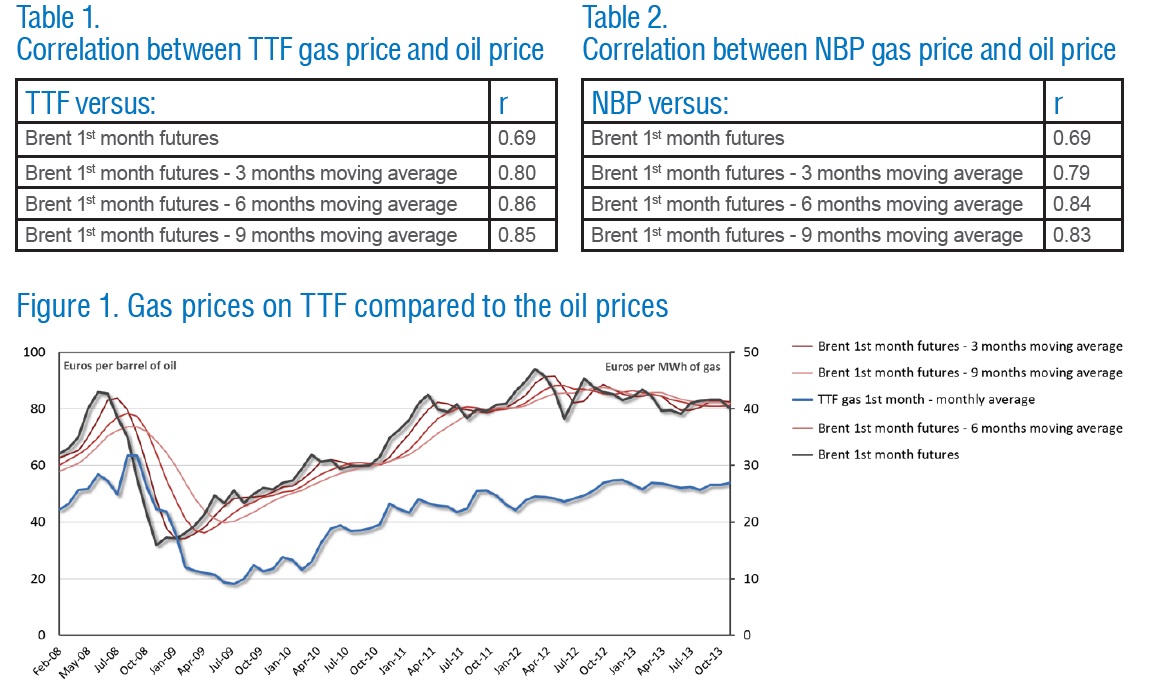

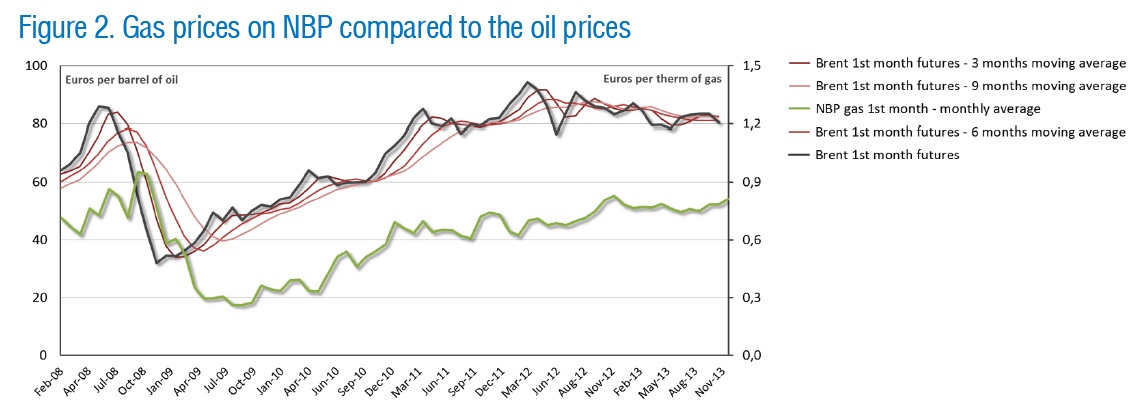

Our recent study provides another argument to back up the conclusion that oil-indexation is still the dominant model of pricing in Europe. In our study, we used gas prices from the front month contracts on the TTF hub and NBP hub. For oil prices, we used prices from the front month contract for Brent on the ICE (London). Monthly average prices were calculated on the basis of Bloomberg’s daily quotations from the beginning of 2008 up until the end of November 2013.

It turns out that the correlation coefficient "r” directly between TTF and Brent and NBP and Brent is 0.69, which is not an indication of weak correlation. But if we look at the 3, 6, and 9 month moving averages for oil prices in our calculations, the results of the study provide strong evidence in favor of robust gas/oil peg.

The correlation is the highest, at 0.86, between the 6 month moving average for oil and TTF. For NBP, the same analysis gives us a correlation of 0.84.

It is precisely this 6 month lag that is most commonly used by major European suppliers in their long-term contracts. Results obtained from the use of moving averages means that forward prices on the hubs are determined by the market participants in the background of the oil-indexed long-term contracts, effectuated, first of all, by Gazprom. Isn’t that a valid testimony for linkage between oil-indexed and hub prices?

More importantly, oil-indexed contract prices are regarded by parties as a benchmark for the entire gas market. In the absence of global price for gas, oil-indexed proxy represents a convenient mechanism for price setting. Many gas buyers and sellers are interested in preserving the current pricing principles because they make gas markets more transparent and predictable.

*Deputy Head of Pricing and Contract Structuring, Gazprom Export

(source: "Blue Fuel", Gazprom Export Global Newsletter, December 2013, Vol. 6, Issue 6)